UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

For the transition period from to

Commission file number

(Exact name of registrant as specified in its charter)

|

|

|

|

||

(State or other jurisdiction of Identification No.) |

|

(I.R.S. Employer incorporation or organization) |

|

|

|

(Address of principal executive offices) |

|

(Zip Code) |

(

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

|

|

Title of each class |

|

Trading Symbol |

|

Name of each exchange on which registered |

|

|

The |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

Smaller reporting company |

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked prices of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter. $

Indicate the number of shares outstanding of each of the registrant’s classes of common shares, as of the latest practicable date.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

|

|

|

|

|

Page |

|

|

|

|

1 |

|

|

|

|

1 |

||

|

|

|

13 |

||

|

|

|

35 |

||

|

|

|

35 |

||

|

|

|

36 |

||

|

|

|

36 |

||

|

|

|

|

37 |

|

|

|

|

37 |

||

|

|

|

37 |

||

|

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

38 |

|

|

|

|

44 |

||

|

|

|

44 |

||

|

|

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

44 |

|

|

|

|

44 |

||

|

|

|

45 |

||

|

|

|

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

45 |

|

|

|

|

|

46 |

|

|

|

|

46 |

||

|

|

|

51 |

||

|

|

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

55 |

|

|

|

|

Certain Relationships and Related Transactions, and Director Independence |

56 |

|

|

|

|

58 |

||

|

|

|

|

60 |

|

|

|

|

60 |

||

|

|

|

65 |

Our consolidated financial statements are stated in United States Dollars and are prepared in accordance with United States Generally Accepted Accounting Principles, or U.S. GAAP.

In this annual report, unless otherwise specified, all dollar amounts are expressed in U.S. dollars.

As used in this annual report, the terms “we”, “us”, “our”, the “Company”, and “Marpai” mean Marpai, Inc., and our wholly owned subsidiaries, Marpai Captive, Inc. (“Marpai Captive”), Marpai Administrators LLC (formerly known as Continental Benefits, LLC) (“Marpai Administrators”), Marpai Health, Inc. (“Marpai Health”), its wholly owned Israeli subsidiary EYME Technologies, Ltd. (“EYME”), and Maestro Health, LLC, unless otherwise indicated or required by the context.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other securities laws. Also, whenever we use words such as “potential,” “possible,” “continue,” “believes,” “intends,” “plans,” “expects,” “estimate,” “may,” “will,” “should,” or “anticipates” and negatives or derivatives of these or similar expressions, we are making forward-looking statements. These forward-looking statements are based upon our present intent, beliefs or expectations, but forward-looking statements are not guaranteed to occur and may not occur. Forward-looking statements are based on information we have when those statements are made or management’s good faith belief as of that time with respect to future events, and are subject to significant risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Important factors that could cause such differences include, but are not limited to:

The foregoing does not represent an exhaustive list of matters that may be covered by the forward-looking statements contained herein or risk factors that we are faced with that may cause our actual results to differ from those anticipated in our forward-looking statements. Please see “Risk Factors” for additional risks that could adversely impact our business and financial performance. Moreover, new risks regularly emerge and it is not possible for our management to predict or articulate all the risks we face, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. All forward-looking statements included in this Annual Report are based on information available to us on the date of this Annual Report. Except to the extent required by applicable laws or rules, we undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained above and throughout this Annual Report.

Part I

ITEM 1. BUSINESS

Our Business

We are a technology-driven healthcare payer, which uses artificial intelligence ("A.I.") and data analytics to help our clients ("Clients") lower their cost of healthcare by enabling better health outcomes for their employees and families. Our mission is to positively change healthcare for the benefit of (i) our Clients who are self-insured employers that pay for their employees’ healthcare benefits and engage us to administer the latter’s healthcare claims, and we refer to them as our “Clients”; (ii) employees and their family members who receive these healthcare benefits from our Clients, and we refer to them as our “Members”, and (iii) healthcare providers including, doctors, doctor groups, hospitals, clinics, and any other entities providing healthcare services or products, and we refer to them as the “Providers.” We are creating the healthcare payer of the future for self-insured employers in the U.S., what we refer to as the “Payer of the Future.” We provide administrative services, and act as Third-Party-Administrator (“TPA”) to self-insured employers who provide healthcare benefits to their employees. Most of our Clients are small and medium-sized companies as well as local government entities. Currently, we have over 200 Clients. We provide services to a total of over 41,000 of our Clients’ employees, and including their spouses and dependents, we serve a total of over 73,000 Members in 44 states in addition to the District of Columbia. As of December 31, 2022, no single Client represents more than 6.2% of our annual revenue.

Industry Trends in the Healthcare Payer

Today, we see some megatrends that enable our market setup.

We, believe that we are uniquely positioned to connect the growing need of the market for VBC contracts with the growing number of providers. Our A.I. platform identifies opportunities and connects members in need with the best possible VBC contract

Key drivers of healthcare cost increases are chronic diseases and various forms of waste.

Chronic diseases — According to the Centers for Disease Control and Prevention (“CDC”), chronic conditions such as diabetes, cardiovascular diseases and pulmonary conditions, account for 75% of the U.S. aggregate spending on healthcare each year. Our Clients’ data also suggest that the cost of care for a Member with a chronic condition, such as diabetes, hypertension, chronic obstructive pulmonary disease (“COPD”) and kidney diseases, is two to four times as much as the average cost of care for one without any chronic conditions. As many chronic diseases can be prevented and managed given early detection, it is vital that a patient who is on a path to develop these chronic diseases be identified and be given preventive care treatments as early as possible.

1

Waste — A survey of 54 peer-reviewed studies found that up to 30% of medical spending is wasted, according to “Waste in the US Health Care System — Estimated Costs and Potential for Savings,” published in the Journal of the American Medical Association (“JAMA”) in October 2019. Among the waste identified, they include:

In our own Clients’ data, we see wide price variations for the same medical/healthcare procedure in the same city of between four and seven times the median cost. According to a study by UnitedHealth in published in May 2019, one of the largest payers in the U.S., reducing the cost variations of common tests could result in an annual saving of $18 billion.

Market Opportunities

The average annual healthcare expenditure is approximately $12,914 per person, according to the CMS as of 2021. 65% of American workers are covered by employer healthcare plans that are self-funded, according to Statistica. Given the number of American workers this implies total spending of $1.4 trillion on healthcare via employer-sponsored self-funded health plans.

Based on our analysis of actual per employee per month (“PEPM”) expenses received by us and the estimated employee lives in self-funded employer health plans of 108 million, according to Statistica, we estimate our total addressable market (“TAM”) to be up to $63 billion. The drivers of the expansion of our TAM are recently acquired products from our acquisition of Maestro Health. These complement the traditional administrative fees, which most TPA’s charge, and enhance our revenue per employee.

Our Recent Acquisition of Maestro Health

On November 1, 2022, we announced the acquisition of Maestro Health. Maestro Health has a very similar business to ours with the core being a traditional third-party administrator (TPA) of healthcare claims for self-funded employers. Maestro Health services over 60 clients who are employers that employ over 20,000 employees. On average, Maestro Health’s clients are similar to our legacy clients in size, and the vast majority of clients were sold via a healthcare broker.

The acquisition brought us several product lines that we previously had in-house.

The additional value added services described above have led Maestro Health to have a higher revenue per member than we have had in the past as we did not have any in-house value added services. Our goal is to market these Maestro Health products to our legacy customer base as well as to new Clients that we will add in the future.

2

Our Flagship Program – Marpai Cares

In 2022, we launched Marpai Cares, which encapsulates our approach: to maximize the value of the self-funded health plan by creating the healthiest member population, given a Client’s budget. We do this for our Clients for a competitive administration fee. Our Clients get much more than the processing of claims for our management fee. They get a healthier employee population.

The key attributes of Marpai Cares include our use of A.I. and other advanced analytics to do the following for the benefit of our Members’ health:

Marpai Cares + Clinical Care Management – Delivering Value for Clients and Members

Matching Members with high-quality providers is a key component of our services. Since we acquired our first healthcare payer, Continental Benefits, in 2021 we expanded their program called TopCare, which found quality providers for Members. In last year’s Annual Report on Form 10-K, we mentioned that we were providing clinical care management services to our Members via a third party, and that at some point we may bring those services in-house. With the acquisition of Maestro Health, we now have a full Clinical Care Management division in-house. This is completely complementary to our approach, and now our own clinical staff can work with legacy and newly-acquired Members.

We continue to identify at-risk members and match them to the right care. We believe the Members with the highest risk are well-known and identified. These are Members who have had or are currently fighting serious conditions. Often these Members, although a small portion of the overall population (e.g. often less than 5% of total Members), can represent a large portion of the total spend for an employer health plan. We address the needs of these Members via active Clinical Care Management, where nurses are making outreaches to them and making sure they have the care they need.

We believe there is an opportunity to deliver better health outcomes for the population as a whole, while containing costs for our clients by also focusing on the next rung of Members at risk. These Members represent “cost bloomers” in that they have similar costs to the average of the plan now, but in the future, they may cost several times the average. This rung of Members often represents a fifth or so of the population. They have complex chronic conditions, multiple comorbidities, and sometimes ignored or misdiagnosed symptoms. These also represent the highest cost Members of the future.

We have deployed our technology to identify these cost bloomers as early as possible. Identification is a critical piece, but we believe engagement with a compelling intervention is what actually drives better outcomes for the Member and lower costs for the Client.

Our Products and Services

We derive our revenues from three general sources: Health Plan Administration Services, ancillary in house services and third party vendor services.

Health Plan Administration

Our current core product and service offering includes handling all aspects of administration related to a healthcare plan. We typically design for our Client a healthcare benefit plan which outlines exactly what coverage the Client would like to provide to its employees.

3

We then manage the plan for the Client by providing the following services:

We do not bear the financial risk with respect to the cost of the claims for any employer. Instead, the self-insured employers and stop-loss insurance companies, if the self-insured employers purchase stop-loss insurance policies to protect themselves from having higher than planned healthcare costs, bear the risk arising from the cost of claims. We sell complementary services to our Clients including care management, case management, actuarial services, health savings account administration and bill review services. Our margin on these partner products varies greatly, but each service makes the overall package for our Clients more complete.

In-House Ancillary Services

Our Ancillary Services revenues include all the revenues that we derive from our inhouse products excluding the administration fees. This revenue is related to products that relate to our role as the administrator of the health plan, but are ancillary to paying claims.

Clinical Care Management - a nurse-led, proactive guide for at-risk members across the care continuum so they get the right high-quality care at the right time and avoid excessive, inappropriate, and overpriced care. Instead of simply treating a condition, they take a personal, holistic approach, to help plan members every step of the way. The ROI on acute case management can be approximately 3x, while it can be 9x for utilization management (pre-authorizations).

Repricing Insights – out-of-network claims are a reality for any health plan. This product encompasses all the negotiation and adjudication related to out of network claims. Clients often save up to 60% on their out-of-network claims versus the initial billed amount.

Marpai PACCS – Pharmacy Advocacy Cost Containment Solution (PACCS) is our member-driven pharmacy savings program that focuses on specialty and high-cost medications to generate up to a 75% savings.

MarpaiRx – our new, national pharmacy benefit management program that saves Clients and Members money and delivers a high-touch Member experience. We grant access to prescriptions at affordable rates and coordinate pharmacy and medical benefits to ensure that the right care is delivered and paid for in a way that reduces the overall cost of healthcare. We are transparent, which means we disclose all rebate information to our clients.

Third Party Services

Some of our revenues were derived from services that were provided to our Clients and Members by third party vendors. We typically pass through most of these revenues to these vendors and their contribution to our gross profit is relatively small. These services include network access fees that are charged by the provider networks (such as Aetna or Cigna) which are used by our Members when they visit network providers (doctors, hospitals etc.) as well as some cost containment services, and other services provided by third party vendors (i.e. not by us).

Our Strategy

Most of our clients are small to medium size businesses that rely on their brokers to select their third party administrators, or their fully insured health plan, usually in a competitive bid process.

We therefore distribute our services primarily via healthcare brokers. In 2021 and 2022, we made significant investments in building our sales and marketing channels. We believe that we have created relationships with some of the largest brokers in America.

4

Our direct sales force focuses mostly on these brokers, and our goal is to participate in as many competitive bids as possible as we believe that this is the best way for us to grow our Client base.

Given the recent acquisition of Maestro Health with its ancillary in-house services, we are also focused on upselling these ancillary services to our legacy customers.

Research and Development – The Future is Value Based Care

We invest resources in research and development. This investment includes hiring and retaining A.I. scientists, product managers, and engineers. In the past, we invested in creating A.I. models that predict costly events in healthcare. In early 2022, we hired Lutz Finger, who was a population health executive at Google. Mr. Finger has focused our research and development efforts on finding cost bloomers, high cost claimants of tomorrow, as well as creating a value-based ecosystem.

Value based care generally means that some or all of the providers’ fees are at risk if certain health outcome improvements do not occur as promised by the provider of the value based care service. In creating a value based ecosystem, we are leveraging the billions of dollars of investment that have taken place over the last years to create remarkable solutions that improve health outcomes.

For example, we have announced a partnership with Virta Health, a company that has one of the longest running trials related to Type 2 Diabetes. Virta Health claims that 94% of Members on the program can end or reduce insulin usage after one year, and 60% of Members can be off all diabetes-specific drugs and living diabetes-free after one year. Virta Health has agreed to work with us in a value based arrangement, which means part of their fees are at risk and dependent on the program working for our Members.

Our role in this value based ecosystem is as an aggregator of lives. Our spending on technology is related to the evolution of our platform, A.I. models and analytics, so we can do the following:

We believe this is the natural evolution of our technology and our unique approach. We will continue to add best-in-class vendors to the ecosystem so long as they are medically vetted and reviewed, have a remarkable Member experience, and have the financial backing to be value based (i.e. put their fees at risk and base them on health outcomes achieved).

We expect that the value based ecosystem will become commercial during 2023. It will expand substantially during the years to come. The fees to our Clients from the vendors are charged as claims to the health plan, and these are all processed by Marpai. We generate revenue through a participation in these fees from the vendor.

Marpai Captive, Inc.

Marpai Captive, Inc. was founded in March 2022 as a Delaware corporation. Marpai Captive is intended to be engaged in the captive insurance market. Marpai Captive commenced operations with a small membership in the first quarter of 2023.

Marpai Health, Inc.

Marpai Health, Inc. (originally named “CITTA, Inc.”) was founded in February 2019 as a Delaware corporation. Together with its wholly owned subsidiary, EYME, founded in March 2019 in Israel, Marpai Health engages in developing and marketing A.I. and healthcare technology to analyze data with the goal of predicting and preventing costly healthcare events related to chronic conditions and expensive medical and surgical procedures.

In August 2019, Marpai Health entered into an asset purchase agreement to acquire a software system and big data analytics platform for research, analysis and prediction of security related events using A.I. for law enforcement agencies (the “Purchased Assets”). In August 2019, in connection with an asset acquisition, Marpai Health issued a convertible note in the principal amount of $2,930,000 (the “SQN Convertible Note”). The purchase price of the Purchased Assets was $3,250,000, consisting of $70,000 in cash, 31,250 shares of Marpai Health’s common stock, and the SQN Convertible Note in the aggregate principal amount of $2,930,000.

EYME serves as Marpai Health’s research and development center with eight employees in Israel. Since its inception through April 1, 2021, the date of the acquisition of Marpai Administrators LLC, (formerly Continental Benefits, LLC), Marpai Health reported no revenues.

Marpai Administrators, LLC (formerly Continental Benefits LLC)

Marpai Administrators was founded in Florida as a limited liability company in November 2013. Marpai Administrators was a wholly owned subsidiary of WellEnterprises USA, LLC which was founded in 2012. Marpai Administrators provides benefits outsourcing services to clients in the U.S. across multiple industries. Marpai Administrators’ backroom administration and TPA services are supported by a

5

customized technology platform and a dedicated benefit call center. Under its TPA platform and TopCare® program, Marpai Administrators provides health and welfare administration, dependent eligibility verification, Consolidated Omnibus Budget Reconciliation Act (“COBRA”) administration, and benefit billing.

In September 2019, Marpai Health began to approach TPAs in an effort to commercialize its technology. Sharing the vision of bringing to market a healthcare “payer of the future” by using advanced A.I. technology in the TPA business, Marpai Health and Marpai Administrators started to have discussions about information exchange, and joint development in December 2019 and Marpai Administrators has been serving as Marpai Health’s A.I. products design partner ever since. In August 2020, Marpai Health started to explore long-term strategic opportunities with Marpai Administrators. In September 2020, the parties entered a letter of intent pursuant to which Marpai Health would acquire Marpai Administrators. On April 1, 2021, pursuant to the terms of the Amended and Restated Equity Interest Purchase and Reorganization Agreement (the “Purchase and Reorganization Agreement”), by and among Marpai, Inc., Marpai Health, all stockholders of Marpai Health, holders of convertible notes of Marpai Health, Marpai Administrators, WellEnterprises USA, LLC and HillCour for the purpose of joinder, to effectuate Marpai, Inc.’s acquisition of Marpai Health and Marpai Administrators, the stockholders of Marpai Health and the sole member of Marpai Administrators contributed their respective securities and ownership interests in Marpai Health and Marpai Administrators to Marpai, Inc. for a combination of shares of Class A common stock and Class B common stock of Marpai, Inc. (the “Acquisition”). Options to purchase 1,027,602 shares of Marpai Health common stock and warrants to purchase 1,366,746 shares of Marpai Health common stock were exchanged, on a one-to-one basis, for options and warrants to purchase shares of our Class A common stock. In addition, pursuant to a Note Exchange Agreement, we issued new notes in the aggregate principal amount of $2,198,459 (the “New Notes”) in exchange for certain then outstanding convertible promissory notes of Marpai Health of equivalent amount of outstanding principal and accrued but unpaid interest. The SQN Convertible Note remained outstanding at the time of the acquisition. The SQN Convertible Note was mostly converted to equity at the Company’s initial public offering ("IPO") and remaining balance was repaid. For details on the Acquisition, see “Item 1. Business — Marpai, Inc.’s Acquisition of Marpai Health and Marpai Administrators (formerly Continental Benefits)” below.

The healthcare industry is highly regulated, and the criteria are often vague, and subject to change and interpretation by various federal and state legislatures, courts, enforcement, and regulatory authorities. Only a treating physician can determine the condition and appropriate treatment for any individual patient. Our future prospects are subject to the legal, regulatory, commercial, and scientific risks.

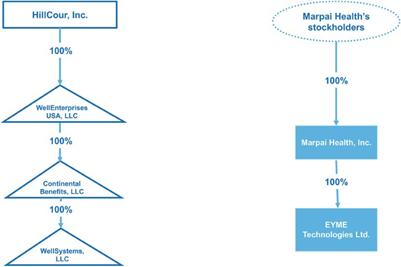

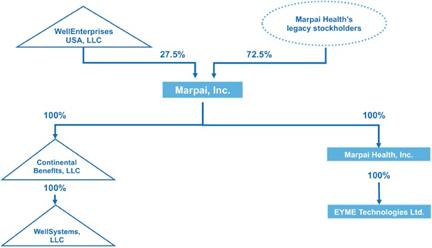

Marpai, Inc.’s Acquisition of Marpai Health and Marpai Administrators (formerly Continental Benefits)

On April 1, 2021, pursuant to the terms of the Purchase and Reorganization Agreement, the stockholders of Marpai Health and Marpai Administrators contributed their respective ownership interests in Marpai Health and Marpai Administrators to Marpai, Inc. for a combination of shares of our Class A common stock and Class B common stock of Marpai, Inc., HillCour and WellEnterprises, LLC agreed to perform certain transition services for us pursuant to a Transition Services Agreement.

The Acquisition was treated as an integrated transaction for U.S. federal income tax purposes and qualified as a tax-free reorganization pursuant to section 351 or 368 of the Internal Revenue Code of 1986, as amended.

The Purchase and Reorganization Agreement required that Marpai Administrators to not have less than $4.762 million of cash on hand, and to have no debt at the time of closing of the Acquisition.

Pursuant to the Purchase and Reorganization Agreement, Marpai Administrators was valued solely for purposes of the Acquisition, on a cash-free and debt-free basis, at $8.5 million. Including the $4.762 million of cash on Marpai Administrators’ balance sheet, equity totaled $13.26 million. In addition, pursuant to Purchase and Reorganization Agreement, Marpai Health was valued solely for purposes of the Acquisition at an assumed pre-money valuation of the last convertible note’s conversion price of $35 million.

As a result of the Acquisition,

6

Pre-Acquisition Entity

Structure

Marpai, Inc.’s Post-acquisition Structure

Effective Time of the Acquisition

The Acquisition became effective on April 1, 2021.

Treatment of Marpai’s Stock Options and Marpai Administrators’ Phantom Units

Each outstanding option of Marpai Health has been assumed by Marpai, Inc. and automatically converted into an option to purchase shares of Marpai, Inc.’s Class A common stock. Prior to the Effective Time, Marpai Administrators and HillCour have discharged all awards of phantom units granted under the Marpai Administrators, LLC Long-Term Incentive Plan. The aggregate value of the discharged phantom unit awards was $1,032,000.

Discharge and Satisfaction of Covered Liabilities

In addition, the seller of Continental, WellSystems, LLC, as well as its owner and affiliate, HillCour, Inc., have agreed to be exclusively responsible for, pay, fully satisfy and otherwise discharge in full certain liabilities that exist as of Closing Date or may arise in the future, related to following categories of events, facts, acts, omissions, circumstances and/or subject matters, and that relate to the period prior to the Closing Date, both known and unknown as of such date:

7

Class B Conversion

On June 28, 2021, Eli David, Yaron Eitan, Edmundo Gonzalez, Grays West Ventures LLC, HillCour Investment Fund, LLC, and WellEnterprises USA, LLC converted an aggregate of 927,817 shares of the Company’s Class B common stock they held into 4,226,968 shares of Class A common stock on a one-to-one basis (“Class B Conversion”). Until the Class B conversion, the Company was authorized to issue two classes of common stock, Class A common stock and Class B common stock. The issued and outstanding shares of Class B common stock were converted into Class A common stock as described above, and the authorized class of Class B common stock was eliminated with the filing of the Second Amended and Restated Charter.

Power of Attorney and Proxy

Concurrently with the Class B Conversion, the Company, (i) HillCour Investment Fund, LLC and WellEnterprises USA, LLC (together, the “HillCour Founding Group”) and (ii) Eli David, Yaron Eitan, Edmundo Gonzalez and Grays West Ventures LLC (collectively, the “Grays Founding Group,” and together with the HillCour Founding Group, the “Co-Founders”) entered into the Power of Attorney and Proxy pursuant to which the HillCour Founding Group granted the Grays Founding Group the right to vote 1,560,237 shares of the Company’s Class A common stock it held (“Proxy Shares”) on all matters relating to any of the following: (i) change to the composition of the Company’s board of directors; (ii) sale of all or substantially all of the Company’s assets or capital stock, or a merger involving the Company; (iii) replacement of the Company’s CEO or other C-level officers; (iv) amendment or approval of any corporate documents or agreements in connection with the Company’s corporate structure or capital raising activities; (v) approval of the Company’s annual budget and business plan; and (vi) the Company’s acquisition, joint venture or other collaborative agreements. Consequently, the HillCour Founding Group and the Grays Founding Group currently have the right to vote 3,913,268 and 3,913,263 shares of the Company’s capital stock, respectively. The Power of Attorney and Proxy also provides that the number of Proxy Shares is subject to adjustment from time to time to maintain as much as possible, equal voting power in the Company between the HillCour Founding Group on the one hand and the Grays Founding Group on the other, subject to certain exceptions related to transfer of shares by the parties.

Pursuant to this Power of Attorney and Proxy, the Co-Founders have also agreed to vote all their shares for the election of (a) Damien Lamendola (or another nominee of the HillCour Founding Group), (b) Edmundo Gonzalez; and (c) Yaron Eitan (or up to two other nominees of the Grays Founding Group) as the Company’s directors. The Power of Attorney and Proxy is irrevocable and will remain in full force and effect until the earlier of (i) consummation of the sale of all or substantially all of the Company’s assets, or the acquisition of the Company by a third party (by way of stock acquisition, merger, recapitalization or otherwise), or (ii) the time when the Grays Founding Group collectively owns fewer than 1,882,420 shares of the Company’s capital stock.

8

Directors and Executive Officers

Pursuant to the terms of the Purchase and Reorganization Agreement, all of the directors of Marpai Administrators resigned. Effective as of the Closing, the combined company’s board of directors was fixed at seven members and comprised of two former members of Marpai Health’s executive management team, four independent directors, and Damien Lamendola, the indirect majority owner of WellEnterprises USA, LLC and HillCour.

Our current management team consists of the following member of the former Marpai Health executive management team:

|

|

|

|

|

Name |

|

Combined Company Position(s) |

|

Position(s) at Marpai Health |

Edmundo Gonzalez |

|

Chief Executive Officer, Secretary, and Director |

|

Co-founder, CEO, and Director of Marpai Health |

Marpai Inc.’s acquisition of Maestro Health, LLC

On August 4, 2022, we entered into a Membership Interest Purchase Agreement (the “Agreement”) with XL America Inc., a Delaware corporation, Seaview Re Holdings Inc., a Delaware corporation (XL America Inc. and Seaview Re Holdings Inc. are collectively referred to herein as the “Equity Sellers”), and AXA S.A., a French société anonyme (the “Debt Seller,” and, together with the Equity Sellers, collectively, the “Sellers”). Pursuant to the terms of the Agreement, we agreed to acquire all of the membership interests (the “Units”) of Maestro Health (the “Maestro Acquisition”). The Equity Sellers owned an aggregate of 100% of the issued and outstanding Units of Maestro Health. The Maestro Acquisition was closed on November 1, 2022.

Maestro Health is a TPA for employee health and benefits, which offers an end-to-end health plan solution, integrating care management and cost containment for its customers. The Agreement contains representations and warranties customary for transactions of this nature negotiated between sophisticated purchasers and sellers acting at arm’s length, certain of which are qualified as to materiality and knowledge and subject to reasonable exceptions. The closing of the Maestro Acquisition was subject to certain customary closing conditions as contained in the Agreement, including: (i) that the Equity Sellers shall have sold, assigned, transferred, conveyed and delivered to the Company all of the Equity Sellers’ rights, title, and interests in and to all of the Units; and (ii) the Debt Seller shall have irrevocably transferred and assigned to us all of the Debt Seller’s rights and obligations with respect to receiving payments under that certain Term Loan Agreement, dated May 11, 2022, by and between the Debt Seller and Maestro Health, in the principal amount of $59,900,000 (the “AXA Note”).

In consideration for our acquisition of the Units, we agreed to pay the Sellers an aggregate purchase price (the “Purchase Price”) of $19,900,000 determined on the closing date (the “Base Purchase Price”), which shall be payable on or before April 1, 2024 (the “Payment Date”), and shall accrue interest until such time that is paid, such that on the Payment Date the Purchase Price, plus all accrued and unpaid interest, shall equal $22,100,000 (for clarity, the Base Purchase Price shall be adjusted, in each case, pursuant to the terms of the Agreement). We agreed to pay the Equity Sellers an amount of $100 with the balance of the Purchase Price to be paid to the Debt Seller for the repayment of the AXA Note. In no event will we be responsible for any further payments for the repayment of the AXA Note other than the repayment of the Purchase Price as provided in the Agreement. Following the Payment Date, any unpaid portion of the Purchase Price shall accrue interest at ten percent (10%) per annum, compounding annually, calculated on the basis of a 365-day year for the actual number of days elapsed (the “Specified Rate”), and shall be repaid as promptly as practicable to the Debt Seller. In addition, in the event we or one of our subsidiaries receive proceeds from the sale of any securities in a private placement or public offering of securities (each an “Offering”), then we shall pay to the Debt Seller an amount equal to thirty-five percent (35%) of the net proceeds of the Offering no later than sixty (60) days after the closing of Offering until such time as the Purchase Price has been paid in full.

Notwithstanding the foregoing, we shall be required to make accumulated annual payments to the Debt Seller, representing the Purchase Price, as follows: (i) $5,000,000 to be paid by December 31, 2024, (ii) $11,000,000 to be paid by December 31, 2025, and (iii) $19,000,000 to be paid by December 31, 2026.

In addition, we are obligated to pay the full amount of any remaining unpaid Purchase Price (inclusive of any accrued interest at the Specified Rate) by no later than year-end 2027, and in no event shall we be required to pay total cash consideration equal to more than the aggregate amount of the Purchase Price (as adjusted pursuant to the terms of the Agreement).

Maestro Health LLC

Maestro Health is a Self-Funded Health Plan service provider which delivers a complete, all-in employee health and benefits solution to brokers, carriers, and employers.

Maestro Health is a Delaware domiciled limited liability company. It was formerly known as Maestro Health Inc., a Delaware domiciled corporation, which was organized on May 2, 2013. Maestro Health, Inc. converted to Maestro Health, LLC effective as of December 17, 2020. Maestro Health’s services help employers control all aspects of the complex employee health and benefits system. Maestro Health owns and operates self-funded insurance administration, benefits administration, enrollment, ACA compliance, consumer directed health care account administration, medical management, and consolidated billing solution applications, unifying them on a single, comprehensive mobile and web platform. In 2021, it added an Out of Network Repricing Solution and an Rx Patient Assistance Program to its service offerings.

Maestro Health’s wholly owned subsidiaries are Integra Employer Health, LLC, Context Benefit Advisors, LLC (formerly Colton Groome Benefit Advisors, LLC), Workable Solutions, LLC, and Group Associates, Inc.

9

Government Regulation

Overview

We believe that our business and operations as outlined above are in substantial compliance with applicable laws and regulations. Only a treating physician can determine if a prediction made by our TopCare® program is correct or appropriate for any individual patient. However, Marpai does not currently share its TopCare® predictions with patients or their providers. Our future prospects are subject to the legal, regulatory, commercial, and scientific risks outlined below and under the section titled, “Risk Factors.”

The healthcare industry is highly regulated and continues to undergo significant changes as third-party payers, such as Medicare and Medicaid, traditional indemnity insurers, managed care organizations and other private payers, increase efforts to control cost, utilization, and delivery of healthcare services. Healthcare companies are subject to extensive and complex federal, state, and local laws, regulations, and judicial decisions.

Additionally, a significant component of Marpai’s services requires the collection and processing of personal information, including protected health information. We collect and may use personal information to help run our business and enable us to provide our services. In some instances, we may use third party service providers to assist us in the above.

Health Care Reform

The Patient Protection and Affordable Care Act ("ACA") was enacted into law in 2010. The provisions of the ACA are comprehensive and varied and are generally directed at implementing health insurance reforms, such as Medicare, Medicaid and the State Children’s Health Insurance Program, to increase health insurance coverage and reduce the number of uninsured and reshaping the health care delivery system to increase quality and efficiency and reduce cost. Certain provisions of the ACA took effect immediately or within a few months, while others will be phased in over time, ranging from one year to ten years. Because of the complexity of health care reform generally, additional legislation is likely to be considered and enacted over time. The ACA, and any subsequent health care reform legislation, will require the promulgation of substantial regulations with significant effect on the health care industry. Thus, the health care industry may be subjected to significant new statutory and regulatory requirements, and consequently to structural and operational changes and challenges, for a substantial period. In addition, there have been judicial and congressional challenges to various elements of the ACA, as well as efforts to modify certain aspects of the ACA.

The implementation of the ACA has changed healthcare financing and delivery by both governmental and private insurers substantially, and affected medical device manufacturers significantly. The ACA, among other things, implemented payment system reforms including a national pilot program on payment bundling to encourage hospitals, physicians and other providers to improve the coordination, quality and efficiency of certain healthcare services through bundled payment models.

Reimbursement

Neither we nor our self-insured clients receive reimbursements from federal health care programs such as Medicare, Medicaid, CHIP, TRICARE and the Veterans Administration. If in the future, we receive reimbursements from these programs, which are subject to complex statutory and regulatory requirements, administrative rulings, interpretations of policy, determinations by fiscal intermediaries and government funding restrictions, all of which would materially increase or decrease reimbursement to our Company.

The process for determining whether a payor will provide coverage for a product is typically separate from the process for setting the reimbursement rate that the payor will pay for the product. A payor’s decision to provide coverage for a product does not imply that an adequate reimbursement rate will be available. Additionally, in the United States there is no uniform policy among payors for coverage or reimbursement. Third-party payors often rely upon Medicare coverage policy and payment limitations in setting their own coverage and reimbursement policies, but also have their own methods and approval processes. Therefore, coverage and reimbursement for products can differ significantly from payor to payor. If coverage and adequate reimbursement are not available, or are available only at limited levels, successful commercialization of, and obtaining a satisfactory financial return on, any product we develop may not be possible.

In the United States, there have been, and continue to be proposed and enacted legislation at the federal and state levels designed to, among other things, bring more transparency to drug pricing, review the relationship between pricing and manufacturer patient programs, reduce the cost of drugs under Medicare, and reform government program reimbursement methodologies for drugs. For example, in July 2021, the Biden administration released an executive order, “Promoting Competition in the American Economy,” with multiple provisions aimed at prescription drugs. In response to Biden’s executive order, on September 9, 2021, the U.S. Department of Health and Human Services (“HHS”) released a Comprehensive Plan for Addressing High Drug Prices that outlines principles for drug pricing reform and sets out a variety of potential legislative policies that Congress could pursue as well as potential administrative actions HHS can take to advance these principles. In addition, the Inflation Reduction Act (“IRA”) passed on August 16, 2022. The IRA, among other things, (1) directs HHS to negotiate the price of certain highly-utilized single-source drugs and biologics covered under Medicare and (2) imposes rebates under Medicare Part B and Medicare Part D to penalize price increases that outpace inflation. These provisions will take effect progressively starting in fiscal year 2023, although they may be subject to legal challenges. It is currently unclear how the IRA will be implemented but is likely to have a significant impact on the pharmaceutical industry. Further, the Biden administration released an additional executive order on October 14, 2022, directing HHS to submit a report within 90 days on how the Center for Medicare and Medicaid Innovation can be further leveraged to test new models for lowering drug costs for Medicare and Medicaid beneficiaries. We expect that additional U.S. federal healthcare reform measures will be adopted in the future, any of which could limit the amounts that the U.S. federal government will pay for healthcare products and services, which could result in reduced demand for our product candidates or additional pricing pressures.

10

Fraud and Abuse

Health care fraud and abuse laws have been enacted at the federal and state levels to regulate both the provision of services to government program beneficiaries and the methods and requirements for submitting claims for services rendered to such beneficiaries. In addition, certain fraud and abuse laws may extend to payer sources other than federal or state-funded programs. Under these laws, individuals and organizations can be penalized for various activities, including submitting claims for services that are not provided, are billed in a manner other than as actually provided, are not medically necessary, are provided by an improper person, are accompanied by an illegal inducement to utilize or refrain from utilizing a service or product, or are billed in a manner that does not comply with applicable government requirements. Both individuals and organizations are subject to prosecution under the criminal and civil fraud and abuse statutes relating to health care providers.

The federal anti-kickback law (the “Anti-Kickback Law”) prohibits, among other things, knowingly and willfully offering or receiving remuneration to induce the referral of items or services that are reimbursable by a federal health care program, or (ii) the purchase, lease, or order of, or the arrangement or recommendation of the purchasing, leasing, or ordering of any item or service reimbursable in whole or in part under Medicare, Medicaid or other federal healthcare programs. The Office of Inspector General has issued a series of regulations, known as the “safe harbors” which immunizes the parties to the business arrangement from prosecution under the Anti-Kickback Law. The failure of a business arrangement to fit within a safe harbor does not necessarily mean that the arrangement is illegal. Many states have adopted laws like the Anti- Kickback Law, and some apply to items and services reimbursable by any payer, including private insurers.

Noncompliance with the Federal Anti-Kickback Statute can result in civil, administrative and/or criminal penalties, restrictions on the ability to operate in certain jurisdictions, and exclusion from participation in Medicare, Medicaid or other federal healthcare programs. In addition, non-compliance can result in the need to curtail and/or restructure operations. Any penalties, damages, fines, exclusions, curtailment or restructuring of operations could adversely affect the ability to operate a business, financial condition, and results of operations. A violation of the Federal Anti-Kickback Statute can serve as a false or fraudulent claim for purposes of the civil False Claims Act and the civil monetary penalties statute.

The so-called Stark Law prohibits physician referrals of Medicare patients to an entity providing certain “designated health services” if the physician or an immediate family member of the physician has any financial relationship with the entity and the financial relationship does not fall within one of the enumerated exceptions to the Stark Law. The Stark Law also prohibits state receipt of federal Medicaid matching funds for services furnished pursuant to a prohibited referral. In addition to the Stark Law, many states have their own self- referral bans, which may extend to all self-referrals, regardless of the payer.

The federal False Claims Act imposes liability for the submission (or causing the submission) of false or fraudulent claims for payment to the federal government, including for certain violations of the Stark Law. The knowing and improper failure to return an overpayment can serve as the basis for a False Claims Act action and Medicare and Medicaid overpayments must be reported and returned within 60 days of identification. Furthermore, violation of the Stark Law also resulted in denial of payment for the underlying testing services. The private parties (known as “qui tam relators”) of the False Claims Act allow a private individual to bring an action on behalf of the federal government and to share in any amounts paid by the defendant to the government in connection with the action. Various states have enacted similar laws modeled after the False Claims Act that apply to items and services reimbursed under Medicaid and other state health care programs, and, in several states, such laws apply to claims submitted to all payers.

The federal Healthcare Fraud Statute prohibits the knowing and willful execution of a scheme to defraud any health care benefit program, including a private insurer. It also prohibits falsifying, concealing or covering up a material fact or making any materially false, fictitious, or fraudulent statement in connection with the delivery of or payment for health care benefits, items, or services. In addition, state analogs often prohibit similar conduct.

The federal False Claims Act also provides that private parties may bring an action on behalf of (and in the name of) the United States to prosecute a federal False Claims Act violation. These qui tam relators may share in a percentage of the proceeds that result from a federal False Claims Act action or settlement. A person or entity found to have violated the federal False Claims Act may be held liable for a per claim civil penalty. For penalties assessed after June 19, 2020, whose associated violations occurred after November 2, 2015, the penalties range from $11,665 to $23,331 for each false claim, plus three times the amount of damages sustained by the government. The minimum and maximum per claim penalty amounts are subject to annual increases for inflation.

Many states have also adopted some form of anti-kickback and anti-referral laws and false claims acts and civil monetary penalties and other fraud and abuse provisions that apply regardless of payer, in addition to items and services reimbursed under Medicaid and other state programs. A determination of liability under such laws could result in fines, penalties, and exclusion, as well as restrictions on the ability to operate in these jurisdictions.

State and Federal Privacy and Data Security Laws

The Health Insurance Portability and Accountability Act of 1996 and its implementing regulations (HIPAA) and the Health Information Technology for Economic and Clinical Health Act of 2009 and its implementing regulations (HITECH) govern the collection, use, disclosure, maintenance and transmission of identifiable patient information (“Protected Health Information” or “PHI”). HIPAA and HITECH apply to covered entities, which may include health plans as well as to those entities that contract with covered entities (“Business Associates”). HITECH imposes breach notification obligations that require the reporting of breaches of “Unsecured Protected Health Information” or PHI that has not been encrypted or destroyed in accordance with federal standards. Furthermore, the regulations established standard data content and format requirements for submitting electronic claims and other administrative health transactions. Health care

11

providers and health plans are required to use standard formats when transmitting claims, referrals, authorizations, and certain other transactions electronically. Business Associates are subject to potentially significant civil and criminal penalties for violating HIPAA.

In addition to HIPAA, we are subject to other state and federal laws and regulations that address privacy, data protection and the collection, storing, sharing, use, transfer, disclosure and protection of certain types of data. Such regulations include the CAN-SPAM Act, the Telephone Consumer Protection Act of 1991, Section 5(a) of the Federal Trade Commission Act, and the California Consumer Privacy Act (“CCPA”), as amended by the California Privacy Rights Act (“CPRA"), which, where applicable, provides consumers with additional privacy rights.

In addition, other federal and state laws afford additional protections to certain categories of sensitive information. Such protections are commonly afforded to substance abuse, mental health, or information concerning certain contagious diseases.

In addition to the federal privacy and security laws and regulations, most states have enacted data security laws, and breach notification laws, governing other types of personal data such as employee and customer information.

State Managed Care Laws

State insurance and managed cared laws and regulations regulate the contractual relationships with managed care organizations, utilization review programs and third-party administrator activities. These regulations differ from state to state, and may contain network, contracting, and financial and reporting requirements, as well as specific standards for delivery of services, payment of claims, and adequacy of health care professional networks. These laws may apply to us in the event we engage in business transactions with state managed care programs.

Corporate practice of medicine and fee-splitting and laws

Many states have laws prohibiting physicians from practicing medicine in partnership with non- physicians, such as business corporations. In addition, many states, including New York, prohibit certain licensed professional, like physicians, from sharing professional fees with non-licensees. As we do not engage in the practice of medicine, we do not contract with licensees to render professional medical services, and we do not split fees with any medical professionals, we do not believe these laws restrict our business. We merely monitor and analyze historical claims data, including our Members’ interactions with licensed healthcare professionals and recommend the most suitable healthcare providers and/or sources of treatment. We do not provide medical prognosis or healthcare. In accordance with various states’ corporate practice of medicine laws and states’ laws and regulations which define the practice of medicine, our call center staff are prohibited from providing Members with any evaluation of any medical condition, diagnosis, prescription, care and/or treatment. Rather, our call center staff can only provide Members with general and publicly available information that is non-specific to the Members’ medical conditions and statistical information about the prevalence of medical conditions within certain populations or under certain circumstances. Our call center staffs do not discuss Members’ individual medical conditions and are prohibited from asking Members for any additional protected health information (PHI) as such term is defined under HIPAA. Our call center staff has been trained and instructed to always inform Members that they are not licensed medical professionals, are not providing medical advice, and that Members should reach out to their medical provider for any medical advice.

However, any determination by a state court or regulatory agency that our service contracts with our clients violate these laws could subject us to civil or criminal penalties, invalidate all or portions of some of those contracts, require us to change or terminate some portions of our business, require us to refund portions of our services fees, and have an adverse effect on our business. Even an unsuccessful challenge by regulatory authorities of our activities could result in adverse publicity and could require a costly response from us. In the event that in the future we will share or allow access by Members to the contents of our alerts or related information, we will endeavor to do so only in full compliance with regulatory requirements, including, potentially, those regulations regarding the corporate practice of medicine, fee- splitting laws, and medical profession regulation.

State Laws Governing Licensure of Healthcare Professionals

State professional licensing boards contain requirements for the licensure of health care professionals and typically require a healthcare professional who is providing professional services in that state to be licensed. Some state licensing boards specifically address the licensure of professionals who are providing services via telephone or other electronic means. The requirements for licensure generally apply where individuals are engaged in a licensed activity. If we elect to hire a licensed professional to engage in a licensed profession, those individuals may be subject to state licensing laws. In addition, hiring licensed professionals may implicate state prohibitions on the corporate practice of medicine.

Finally, as a TPA, we must maintain active TPA licenses in all states that are not expressly exempt from requiring a TPA license where we conduct business.

Employees

As of December 31, 2022, we have a total of 303 full-time employees, with 15 of them located in Tel Aviv, Israel. None of them are parties to any labor agreements or are represented by a labor union.

Competition

12

Although we believe that the services we offer our Clients are highly differentiated, we operate in a highly competitive market. We only provide administrative services to self-insured employers who provide healthcare benefits to their employees. These self-insured employers can always elect to abandon self- insurance and simply buy medical insurance from one of the large players such as, Aetna, Cigna, or United Healthcare. There can be no assurances that our Clients or prospective Clients will remain self-insured for any given period. If the number of employers which choose to self-insure declines, the size of our targeted market will shrink.

Also, there are other technology-driven companies focused on creating a TPA business among self- insured employers. Like us, they provide machine learning predictions models targeted at measuring risks for Members, identifying members susceptible to adverse healthcare events before they occur, and provide proactive guidance for preventive care. We compete with almost 1,000 TPAs, all of whom are vying for the same business — the management of healthcare benefits for self-insured employers. There is only one TPA at a time for every employer wanting to provide health benefits via a self-insured model, and an employer may remain with the same TPA for many years. This means that although the market is very large, not all of it is accessible by us in any one year. In addition to the very large health insurance companies, there are new players in the market such as Collective Health, Bind Health Insurance, Bright Health Group (NYSE: BHG), Oscar Health, Inc. (NYSE: OSCR) and Centivo, which have all raised substantial venture capital funds, are pursuing a similar strategy to ours, and share our vision to use technology to transform the healthcare payer space. We believe that like us, Collective Health and Clover Health are also targeting at self-insured employers. Although all of them are relatively young companies, they have products in the market already and are known to provide technology- driven TPA services. These companies claim to save employers money and also claim to have high retention rates.

Some of the competitors named above perform care management functions as part of their offerings. Currently, we offer this function through our strategic partners. In the future, we may bring this function in- house. We believe our A.I.-enabled predictions further differentiate our solution by being able to steer Members to the appropriate healthcare Provider sooner. The ultimate gauge of success in our market will be who can help employers reduce the growth of long-term healthcare spending while also improving the quality of healthcare solutions.

Impact of COVID-19 and Macroeconomic Conditions

We continue to monitor the effects of the global coronavirus pandemic outbreak, ("COVID-19") and the global macroeconomic environment, including increasing inflationary pressures; supply chain disruptions; social and political issues; regulatory matters, geopolitical tensions; and global security issues. We are also mindful of inflationary pressures on our cost base and we are monitoring the impact on customer preferences.

Available Information

Additional information about us is contained on our Internet website at www.marpaihealth.com. Information on our website is not incorporated by reference into this Annual Report. Under the “SEC Filings” and “Financial Information” sections, under the “Investors & Media” section of our website, we make available free of charge our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934, as amended, ("the Exchange Act"), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Our reports filed with the SEC are also made available on the SEC’s website at www.sec.gov. The following Corporate Governance documents are also posted on our website: Code of Ethics and the Charters for each of the Committees of our Board of Directors, ("Board").

ITEM 1A. RISK FACTORS

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report, before making a decision to invest in our Class A common stock. The risks and uncertainties described below may not be the only ones we face. If any of the risks actually occur, our business, results of operations, financial condition and prospects could be harmed. In that event, the trading price of our Class A common stock could decline, and you could lose part or all your investment. Some of the statements in “Item 1A. Risk Factors” are forward-looking statements. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business, prospects, financial condition, and results of operations.

Summary Risk Factors

Our business is subject to numerous risks and uncertainties that you should consider before investing in our company. You should carefully consider the risks described more fully below before making a decision to invest in our Class A common stock. If any of these risks occurs, our business, financial condition and results of operations would likely be materially adversely affected. These risks, include, but are not limited to, the following:

13

14

Risks Related to Managing and Growing Our TPA Business

We have relatively limited experience with our A.I. powered TopCare program®, and initial results may not be indicative of future performance.

Sale of products and services through Marpai Administrators’ TopCare® program is key to our success. We believe that our A.I. models with deep learning functionality and predictive algorithms give us the ability to predict chronic conditions and costly medical procedures, and these factors differentiate us from other TPAs. In January 2021, our A.I.- powered TopCare program® went live, making it possible for us to offer our members care management with high-impact predictions. Although our A.I. technology has not yet been integrated with any of our TPA business’ core systems, other than TopCare, to date, we plan to use A.I. in virtually every part of our TPA business.

We currently project that we will need additional capital to fund our current operations and capital investment requirements until we scale to a revenue level that permits cash self-sufficiency. As a result, we need to raise additional capital or secure debt funding to support on-going operations until such time. This projection is based on our current expectations regarding revenues, expenditures, cash burn rate and

15

other operating assumptions. The sources of this capital are anticipated to be from the sale of equity and/or debt. Alternatively, or in addition, we may seek to sell assets which we regard as non-strategic. Any of the foregoing may not be achievable on favorable terms, or at all,. Additionally, any debt or equity transactions may cause significant dilution to existing stockholders.

If we are unable to raise additional capital moving forward, its ability to operate in the normal course and continue to invest in its product portfolio may be materially and adversely impacted and we may be forced to scale back operations or divest some or all of its assets.

There can be no assurances as to how long it will take for our A.I.- powered TopCare program® to resonate with Marpai Administrators’ current Clients, or at all. Even with interested Clients, it will likely take some time for the TopCare® program to yield measurable results.

The audited consolidated financial statements for the year ended December 31, 2022 include an explanatory paragraph in our independent registered public accounting firm’s audit report stating that there are conditions that raise substantial doubt about our ability to continue as a going concern.

As of December 31, 2022, we had an accumulated deficit of $48.0 million and working capital of $9.2 million. As of December 31, 2022, we had $20.2 million of debt and $13.8 million of unrestricted cash on hand. For the year ended December 31, 2022, we recognized a net loss of $26.5 million and negative cash flows from operations of $35.2 million. Since inception, we have met our cash needs through proceeds from issuing convertible notes, warrants and our IPO and we expect that we will need to meet its future cash needs by raising debt, issuing equity and selling assets. Our independent registered public accounting firm, UHY LLP, has included an explanatory paragraph in their audit report that accompanies our audited consolidated financial statements as of and for the year ended December 31, 2022, stating that there are conditions that raise substantial doubt about our ability to continue as a going concern.

Management continues to evaluate funding alternatives and currently seeks to raise additional funds through the issuance of equity or debt securities, through arrangements with strategic partners or through obtaining credit from financial institutions. As we seek additional sources of financing, there can be no assurance that such financing would be available to us on favorable terms or at all. The Company is also considering disposing of what it considers non-strategic assets.

If we are unable to raise additional capital moving forward, our ability to operate in the normal course and continue to invest in our product portfolio may be materially and adversely impacted and we may be forced to scale back operations or divest some or all of our assets.

As a result of the above, in connection with our assessment of going concern considerations in accordance with Financial Accounting Standard Board’s (“FASB”) Accounting Standards Update (“ASU”) 2014-15, “Disclosures of Uncertainties about an Entity’s Ability to Continue as a Going Concern,” management has determined that our liquidity condition raises substantial doubt about our ability to continue as a going concern through twelve months from the date these consolidated financial statements are available to be issued. These consolidated financial statements do not include any adjustments relating to the recovery of the recorded assets or the classification of the liabilities that might be necessary should we be unable to continue as a going concern.

Marpai Administrators has a high annual customer attrition rate historically. The loss, termination, or renegotiation of any contract with Marpai Administrators’ current Clients could have a material adverse effect on our financial conditions and operating results.

Marpai Administrators’ largest two Clients collectively represented approximately 12.1% and 8.0% of its total gross revenue in 2021 and 2022, respectively. For the twelve months ended December 31, 2022 and 2021, its customer attrition rates were approximately 32.9% and 25.0%, respectively. We believe many Clients left due to poor customer service. Although we believe many root causes driving customer attrition have been identified, remedial actions are still in process, there is no assurance that we will be able to reduce the attrition rates going forward. If the high customer attrition rate continues, our future revenue growth will suffer and our operating results will be negatively impacted, and we may encounter difficulty in recruiting new clients due to erosion of customer confidence.

Marpai Administrators is party to several disputes and lawsuits, and we may be subject to liabilities arisen from these and similar disputes in the future.

In the normal course of the claims administration services business, we expect to be named from time to time as a defendant in lawsuits by the insureds or claimants contesting decisions by us or our Clients with respect to the settlement of their healthcare claims. Marpai Administrators’ Clients have brought claims for indemnification based on alleged actions on its part or on the part of its agents or employees in rendering services to clients. We are subject to several disputes and lawsuits of which Marpai Administrators is currently a subject. Any future lawsuits against us can be disruptive to our business. The defense of the lawsuits will be time-consuming and require attention of our senior management and financial resources, and there can be no assurances that the resolution of any such litigation will not have a material adverse effect on our business, financial condition, and results of operations.

Even though pursuant to the Purchase and Reorganization Agreement, WellEnterprises USA, LLC, has agreed to assume all liabilities of Marpai Administrators that relate to benefits claims in excess of $50,000 or that have been outstanding more than 180 days, in each case as of April 1, 2021, Marpai Administrators will ultimately be responsible for any damages that may arise from these lawsuits. To the extent that WellEnterprises USA, LLC is unable or unwilling to satisfy any such liabilities, we will be required to do so. One of our directors, Mr. Damien Lamendola is the majority shareholder of HillCour Holding Corporation, which owns HillCour.

Pursuant to the Purchase and Reorganization Agreement, $500,000 was deposited into an escrow account on April 30, 2021 to indemnify parties for fraud, breach of any representation or warranty, breach or non-performance of any post-closing covenant or agreement.

16

However, there can be no assurances that future lawsuits may not arise. If we are exposed to liabilities more than the amount held in escrow, our financial condition can be materially adversely affected. See “Item 1. Business — Marpai, Inc.’s Acquisition of Marpai Health and Marpai Administrators” “Business — Marpai, Inc.’s Acquisition of Marpai Health and Marpai Administrators.”

If our TopCare® program fails to provide accurate and timely predictions, or if it is associated with wasteful visits to Providers or unhelpful recommendations for Members, then this could lead to low customer satisfaction, which could adversely affect our results of operations.

When our A.I. models make a prediction, we advise the Member to reach out to his or her primary care physician or make suggestions to the Member on the best providers in the area via our TopCare® program since we do not provide medical prognosis. However, Members may not follow our advice or accept our suggestions. We believe that not taking our recommendations will lead to higher claims costs to our Clients. If claim costs remain the same or are not lower than those before we were hired, our Clients may be dissatisfied with our services, terminate or refuse to renew contracts with us.

In addition, our A.I. models may not always work as planned, and the predictions could have many false positives. These errors may lead to wasteful visits to the Providers, Clients’ dissatisfaction and attrition, which may lead to loss of revenue. Our economic models assume that the costs stemming from these false positives is a small fraction of the total savings that may be achieved by preventing or better managing chronic conditions and steering Members who will have high-cost medical procedures to high-quality, lower cost providers. This assumption, however, has yet to be proven. To date, we have no actual case data to support this assumption.

Issues in the use of A.I., including deep learning in our platform and modules could result in reputational harm or liability.

As with many developing technologies, A.I. presents risks and challenges that could affect its further development, adoption, and use, and therefore our business. A.I. algorithms may be flawed. Datasets may be insufficient, of poor quality, or contain biased information. Inappropriate or controversial data practices by data scientists, engineers, and end-users of our systems could impair the acceptance of A.I. solutions. If the recommendations, forecasts, or analyses that A.I. applications assist in producing are deficient or inaccurate, we could be subjected to competitive harm, potential legal liability, and brand or reputational harm. Some A.I. scenarios could present ethical issues. If we enable or offer A.I. solutions that are controversial because of their purported or real impact on human rights, privacy, employment, or other social issues, we may experience brand or reputational harm.

If the markets for our A.I. modules and TopCare® program fail to grow as we expect, or if self — insured employers fail to adopt our TopCare® program and A.I. modules, our business, operating results, and financial condition could be adversely affected.

It is difficult to predict self-insured employer adoption rates and demand for our A.I. modules and TopCare® program, the entry of competitive platforms, or the future growth rate and size of the healthcare technology and TPA markets. We expect that a significant portion of our revenue will come from our A.I. modules with deep learning functionality and predictive algorithms and our TopCare® program. Although demand for healthcare technology, deep learning (an advanced form of A.I.), and data analytics platforms and A.I. applications has grown in recent years, the market for these platforms and applications continues to evolve. There can be no assurances that this market will continue to grow or, even if it does grow, that Clients will choose our A.I. modules, TopCare® program, or platform. Our future success will depend largely on our ability to penetrate the existing market for healthcare technology driven by TPAs, as well as the continued growth and expansion of what we believe to be an emerging market for healthcare administration focused on A.I. platforms and applications that are faster, easier to adopt, and easier to use.